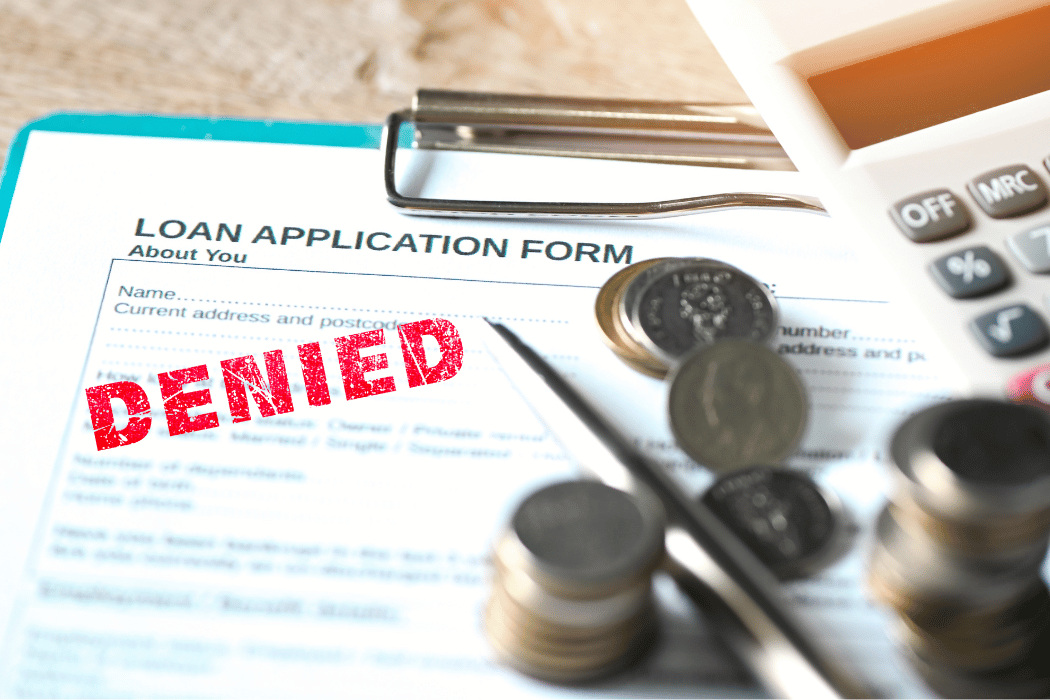

Access to capital remains one of the most critical challenges facing small business owners, but new data reveals a troubling reality: the playing field is far from level when it comes to securing financing. According to a comprehensive LendingTree study analyzing Federal Reserve data on small business lending in 2024, significant disparities persist along racial and ethnic lines, painting a stark picture of the barriers minority entrepreneurs continue to face.

The Numbers Tell a Sobering Story

The data is unambiguous in revealing persistent inequities in business lending. According to the LendingTree study, Black-owned businesses experienced a staggering 39 percent denial rate when applying for loans, lines of credit, or merchant cash advances in 2024 – more than double the 18 percent denial rate faced by white-owned businesses. This disparity represents one of the most significant gaps in the lending landscape, with Black entrepreneurs facing rejection at rates that far exceed any other demographic group.

Hispanic-owned businesses also encounter substantial obstacles, with a 29 percent denial rate that significantly exceeds the national average of 21 percent, the LendingTree research found. Even Asian-owned businesses, with a 24 percent denial rate, face higher rejection rates than their white counterparts. These statistics underscore how minority entrepreneurs must navigate additional hurdles when seeking the capital necessary to launch, sustain, or grow their ventures.

A Complex Web of Contributing Factors

The denial rate disparities reflect a complex intersection of systemic challenges that minority business owners face. Historical barriers to wealth accumulation have left many minority entrepreneurs with less personal capital to invest in their businesses and fewer assets to offer as collateral. Additionally, credit histories may be impacted by broader economic inequalities, creating a cascade effect that influences lending decisions.

The LendingTree data also reveals that smaller businesses face higher denial rates overall, with companies employing one to four people experiencing a 26 percent denial rate compared to just 5 percent for larger firms with 50-499 employees. Since minority-owned businesses are more likely to be smaller operations, this size bias compounds the existing racial disparities in lending.

Industry and Revenue Patterns

The challenges extend across various business sectors, with retail businesses facing the highest denial rates at 25 percent, followed by leisure and hospitality at 24 percent. These industries, which have significant representation among minority-owned businesses, face particular headwinds in securing financing.

Revenue patterns also play a crucial role, with businesses earning $50,001 to $100,000 annually experiencing the highest denial rates at 35 percent. This revenue bracket often represents growing small businesses that are beyond the startup phase but haven’t yet achieved the scale that makes them attractive to traditional lenders.

Gender Gaps Present a Different Picture

Interestingly, the gender gap in lending presents a more nuanced picture. Women-owned businesses actually experienced slightly lower denial rates at 18 percent compared to 21 percent for men-owned businesses. However, this statistic should be interpreted carefully, as it may reflect differences in application patterns, loan amounts sought, or business types rather than indicating an absence of gender-based barriers in entrepreneurship and financing.

The Path Forward

The lending landscape’s disparities have real-world consequences for economic growth and innovation. When minority entrepreneurs face barriers to capital access, entire communities miss out on job creation, innovation, and economic development. The 39 percent denial rate for Black-owned businesses represents not just individual setbacks, but a systemic limitation on economic opportunity and wealth building within minority communities.

Financial experts recommend that minority business owners focus on building strong credit profiles, developing comprehensive business plans with realistic financial projections, and exploring alternative lending sources beyond traditional banks. Credit unions, community development financial institutions, and online lenders may offer different perspectives on creditworthiness and risk assessment.

Looking Ahead

While the overall denial rate remained relatively stable at 21 percent in 2024, the persistent racial disparities in lending decisions highlight the need for continued attention to equitable access to capital. As interest rates have begun to moderate slightly from recent peaks, with median fixed rates dropping to 7.4 percent in early 2025, the focus must shift to ensuring that all qualified business owners can benefit from improved lending conditions.

The data serves as a crucial reminder that achieving true economic equality requires addressing the systemic barriers that prevent minority entrepreneurs from accessing the capital they need to build successful businesses and contribute to economic growth in their communities.