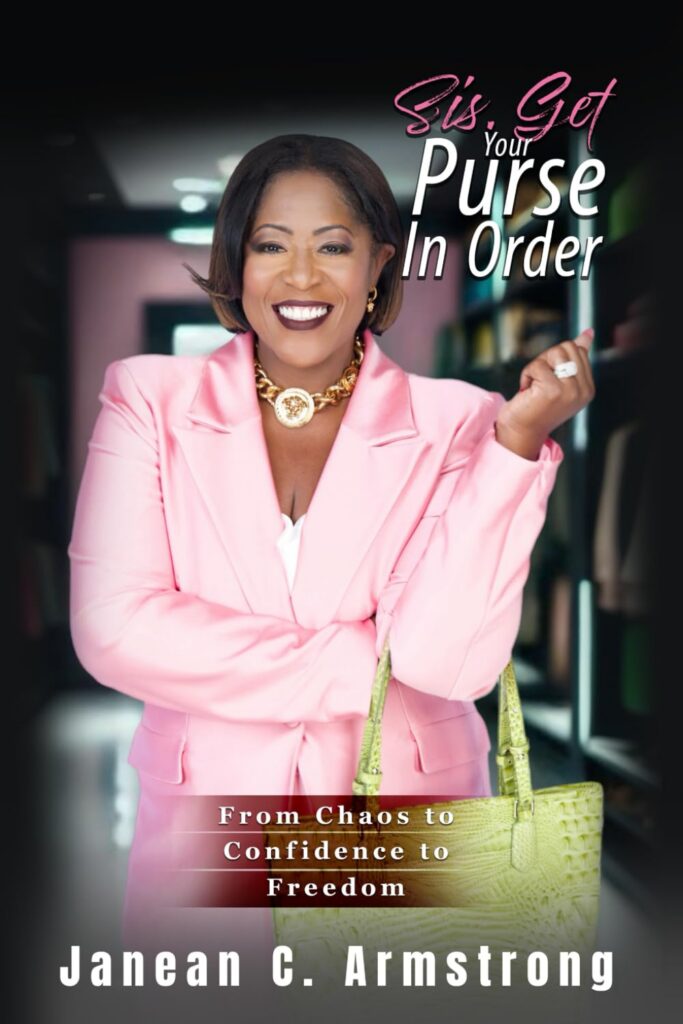

Janean Armstrong spent 30 years learning the secrets of wealth in corporate boardrooms. Now she’s helping women everywhere take control of their money—one purse at a time.

The conversation started on a back porch in Arkansas. Wine glasses clinked. Laughter filled the air. Then Janean Armstrong asked the question that changed everything: “Why don’t we talk about our money?”

Silence.

These were successful women—doctors, executives, entrepreneurs. They shared stories about their husbands, their children, their careers. But when it came to their finances, shame kept them quiet.

One friend finally broke the silence. “I’m ashamed,” she admitted. “I’m highly educated, but my purse is not in order.”

That moment became the seed for Armstrong’s book, “Sis Get Your Purse in Order,” a guide to financial empowerment for women that strips away the shame and replaces it with practical action.

From Small Town to Big Lessons

Armstrong grew up in Halley, Arkansas, a town so small that 400 people felt like a crowd. Most of them were her family. Money conversations didn’t happen there.

What she saw instead was survival. Her grandmother would charge eggs and milk at the local drugstore between Social Security checks. An old white man came around every month to collect $10 for an insurance policy. Armstrong never saw again after her grandmother passed in 2014.

“At the time, I didn’t realize that was a vicious cycle,” Armstrong says.

College brought new challenges. Armstrong left school with a bachelor’s degree in business management and 10 credit cards. She had charged her way through homecoming outfits and campus life. When she applied for her first car loan at 23, the dealer mentioned something called a FICO score. Hers was around 500.

“What’s a FICO score?” she asked.

She had a degree in management but nobody had taught her about credit.

That changed when she entered banking in 1997. For nearly 30 years, she sat in executive boardrooms and C-suites, watching how wealth really worked. She learned the language of money. She understood credit, debt, investment strategies, and emergency savings. She climbed out of her own $10,000 hole, the debt from those 10 college credit cards, and it took her a decade to do it.

Why Financial Literacy for Women Matters More Than Ever

In 2024 and 2025, over 300,000 Black women lost their jobs due to a combination of heavy federal sector job cuts, the dismantling of corporate DEI programs, rising inflation, and the impact of tariff policies on small businesses. Many of them were not prepared.

Armstrong felt her silence becoming selfish. She had the knowledge. She had lived through financial chaos and come out stronger. She knew what worked.

“My silence was being selfish,” she says. “It’s time for me to help my sisters get their purses in order.”

The numbers tell a hard truth. Sixty percent of American families don’t have $1,500 saved for emergencies. Yet credit card interest rates have climbed to 27 to 29 percent. A $1,000 balance carried month-to-month becomes a trap that’s hard to escape.

Armstrong sees the pattern everywhere. Women carry designer purses but have no emergency savings. They swipe cards at checkout and hope they go through, then face crushing interest at the end of the month.

The Three Financial Mistakes Women Make Most

1. Chasing Social Media Dreams

Social media has women in a chokehold, Armstrong says. The glamorous life looks real. The spring and summer collections feel necessary. Keeping up becomes expensive.

What social media doesn’t show is how to build a budget, save for emergencies, or plan for financial freedom. It shows the purse, not what’s inside it.

2. Missing Emergency Savings

Armstrong recommends at least six months of mortgage and car payments saved. She knows that’s a lot. Start with three months if needed. She recently reached a full year of savings herself.

“If I just get tired and say, ‘I have to go, I’m tired of these people,’ I can walk away,” she says. “That’s the freedom I have.”

One late mortgage payment can drop a credit score 100 points. It takes almost a year to recover from that damage. Emergency savings protect against that disaster.

3. Treating Credit Like Extra Money

Credit is a tool, not a paycheck. Armstrong is clear about this rule: If you don’t have the cash, don’t swipe the card. If you can’t pay it off by month’s end, save for it first.

Business Credit vs Personal Credit: Keep Church and State Separate

For entrepreneurs, Armstrong has one rule: Keep business credit and personal credit completely separate. She calls it “church and state.”

When you mix them, business expenses increase your personal debt-to-income ratio. That makes it harder to buy a house, refinance a car, or get approved for personal loans.

Build a strong business credit score by putting everything in your business name. Use your EIN number. Get one or two business credit cards and pay them off every month with your accounts receivable. This keeps your business credit score healthy and your personal credit report clean.

You can check your business credit score through TransUnion, Experian, and Equifax using your EIN number. Pull that report. Review it. Understand your ranges just like you would with personal credit.

Your personal credit still serves as a guarantor when you apply for business loans. But if you keep the accounts separate, defaults only affect your personal score if you guaranteed the business account. Everything else stays clean.

Credit Score Improvement: The Step-by-Step Fix

Armstrong rebuilt her own credit from a 500 FICO score. She knows the way out.

Understand utilization. Your revolving credit is the biggest part of your credit score. If you have a $1,000 credit limit, only use $300. Keep utilization under 30 percent.

Lower utilization raises your score. Higher utilization drags it down. A card maxed out at 92 percent utilization will tank your score. Pay that one down first. Watch your score climb.

Attack high balances first. Pull your credit report. Look at the utilization percentages. If one card shows 92 percent and another shows 14 percent, pay down the 92 percent card first. That will have the biggest impact on your score.

Don’t miss mortgage payments. A missed credit card payment hurts, but you can bounce back in three months. A missed mortgage payment drops your score 100 points or more and takes almost a year to fix.

This is why emergency savings matter. Even if you lose your job, you can keep paying the mortgage. You can use credit cards for other expenses if needed but protect that mortgage payment.

Budgeting for Women: Small Sacrifices, Big Wins

Armstrong includes budgeting workbooks in her book because budgets are where financial empowerment begins.

Start with what you know. Mortgage or rent. Car payment. Utilities. Those are fixed. Put them on auto-draft so they never get missed.

Then budget the variables. Food, both groceries and takeout, might be $400 a month. Entertainment, like brunch with friends, might be $100. Clothing gets a budget only when you have a trip or work event coming up.

The key is sticking to it. Armstrong tells the story of the brunch friend who ordered a salad, ate from everyone’s plates, then complained when the bill got split evenly.

“She really didn’t have the budget to be out there,” Armstrong says. “But you can budget for those moments. Save $20 a week. Set up automatic transfers from checking to savings. Don’t touch it. When it’s time for brunch, you have your $100. Go have your good time. You deserve it. Just don’t eat off everybody’s plate.”

Armstrong warns against stress shopping. After her father passed in 2024, she found herself late at night, scrolling Amazon, clicking through grief. A week later, 20 boxes showed up at her door. Her daughter sent a photo: “Mama, we’re going to have to talk when you get home.”

She returned most of it. Now she knows to find other ways to occupy her mind when emotions run high.

Check subscriptions monthly. Those late-night free trials add up. Cancel what you’re not using. Save those dollars.

Celebrate small wins. When you stick to your budget for a month, treat yourself. Maybe it’s that second Starbucks coffee you sacrificed all month. Maybe it’s something small. The point is to celebrate progress, not punish yourself for wanting financial freedom.

From Shame to Financial Independence: Changing the Conversation

Armstrong’s doctor friend said it best: “I have all these degrees. I’m a doctor. I should know this.”

Armstrong pushed back. “When I go to my doctor with knee problems, I don’t say I’m ashamed I didn’t know that because I have a bachelor’s degree in business management. Medical is not my expertise. Finance is not your expertise. We have to move away from the shame.”

That’s the shift Sis Get Your Purse in Order creates. It’s between you and your purse. No judgment. No shame. Just practical steps, words of affirmation, and workbooks that guide women toward financial independence.

Armstrong is clear: It’s not the designer purse you carry that matters. It’s what’s inside your purse. The budget. The emergency savings. The credit score that opens doors instead of slamming them shut.

Your Purse, Your Purpose, Your Power

The book is available on Amazon, Barnes & Noble, and Books-A-Million in paperback, Kindle, and hardback. You can also find it at www.getyourpurseinorder.com.

Armstrong’s message is simple but powerful: This is your time. Whether you’re married, single, divorced, or widowed, your financial empowerment starts with one decision, to stop being ashamed and start being informed.

She spent 30 years behind the curtain, learning how wealth works in executive boardrooms. Now she’s pulling back that curtain for every woman who wants dignity and freedom with her money.

“If you want your life to change from chaos to confidence, to freedom,” Armstrong says, “this is your time, sis.”